What should you keep in mind when dealing with international buyers and sellers?

Published

Harriet Holmes

Senior AML Enablement and Product Assurance Manager

According to Land Registry data, nearly a quarter of a million properties in the UK are registered to overseas buyers, compared with fewer than 88,000 in 2010. There is nothing inherently wrong with foreign ownership and we shouldn’t be immediately suspicious of foreign buyers. But research from Transparency International has found £4.4 billion worth of property across the UK was bought with suspicious wealth – one fifth by individuals from Russia. Which demonstrates that the risk is not inconsequential.

What are the red flags you should be looking out for?

When dealing with property transactions involving international buyers, it is important to be aware of potential red flags. These can include:

Sudden changes in the finances of the buyer.

Multiple payments from different accounts.

Funds being sent from a foreign country when there is no apparent connection between the country and the client.

The buyer's lack of knowledge about the local property market.

Inconsistencies in customer details, identification and signatures.

High-risk jurisdictions.

Canned or scripted communication from the client.

The client has no significant dealings in the country in which the professional or financial services are sought.

It is also essential in transactional matters that the professional is aware of the buyer's source of funds, as this can often be a sign of suspicious activity.

What are the most significant risks with an international client?

The most significant risk is often distance. Not getting the opportunity to meet the client or see physical documents. If a client is overseas, it is unlikely that you will meet the client in person during the transaction's lifetime. And working in different time zones can mean that communication can be limited to email, making it more difficult to pick up on red flags you may pick up on when meeting the client face to face.

The second significant risk is different countries' nuances. This could be in regard to official documentation or addresses. It is unrealistic to expect our staff to be specialists in every jurisdiction where a client might reside. The professional often lacks specific jurisdictional knowledge, which would ordinarily support identifying red flags.

Reliance on overseas third parties

When dealing with international clients, it is important to be aware of the risks associated with relying on third parties in other countries. This reliance can increase the risk of fraudulent activity and can mean that documents or information may be delayed or incorrect. It is important to understand the local laws and regulations of the country in which the third party is located, and to ensure that all applicable due diligence is completed. Additionally, it is important to ensure that the third party is reputable and experienced in the field, and that the certification process is understood and adhered to.

What are the alternatives to relying on a notary based overseas?

For some international jurisdictions, high-quality data sources enable electronic verification of a client's residential address. This helps to identify any inconsistencies in the client's details and whether they reside in a high-risk jurisdiction, without relying on an overseas third party with which you may have no prior knowledge.

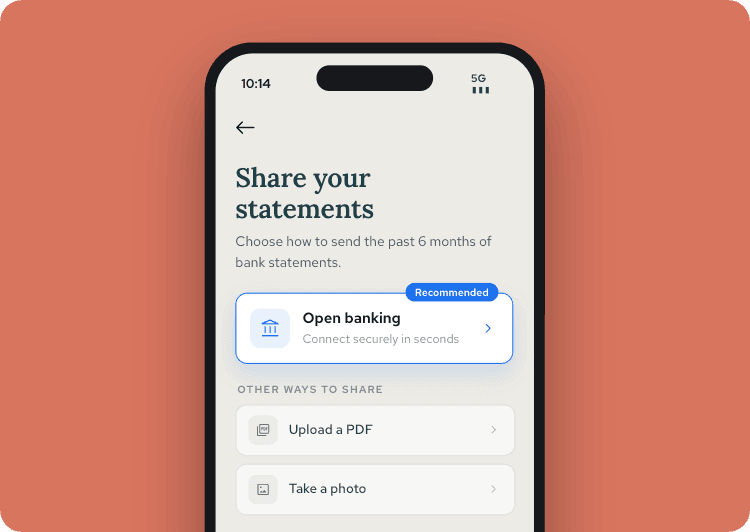

Of course, that is not the end of your due diligence. Depending on the level of risk identified and the content of your firm-wide, client and matter risk assessments, you should look to gather additional evidence which could highlight other red flags. In transactional matters, analysing your client's source of funds is a key part of this, and there is potential that technology can help here, too. Utilising open banking can ensure that bank statements come directly from the bank and are not doctored. Additionally, you can request that additional evidence be sent securely rather than downloading documents via email.

More than 950 regulated businesses rely on Thirdfort. To find out how we can help protect you from criminals living overseas, get in touch.

Subscribe to our newsletter

Subscribe to our monthly newsletter for recaps and recordings of our webinars, invitations for upcoming events and curated industry news. We’ll also send our guide to Digital ID Verification as a welcome gift.

Our Privacy Policy sets out how the personal data collected from you will be processed by us.